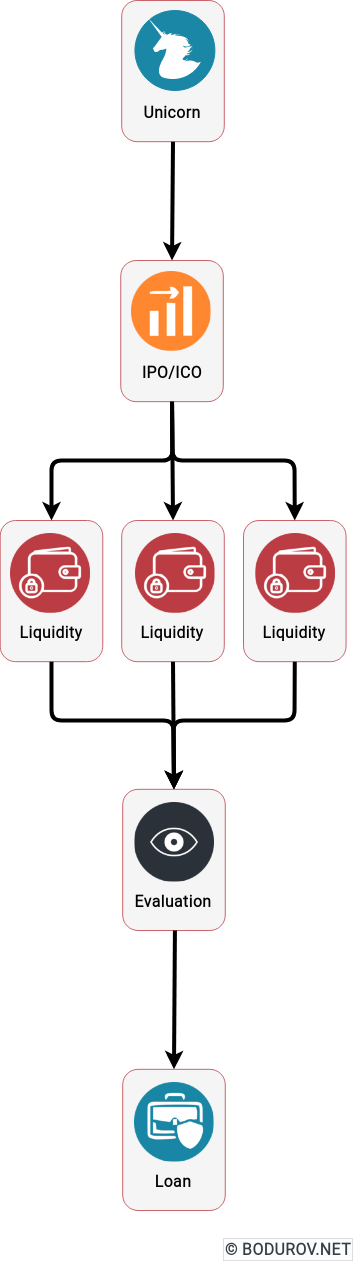

In my article on start-up unicorns, I already presented how most start-ups finance their operations and how efficient this way of work is. This article will show how companies and wealthy individuals finance their operations once they reach unicorn status and have already managed to execute a successful IPO or ICO.

But before explaining the financial workflow, let’s analyze what an IPO is and how it integrates with the standard capitalism-based system. At its core, IPO operates the same way as every ordinary bank. People trust the company doing IPO and are willing to buy common stocks of this company. Additionally, let’s analyze a little bit how banks evaluate a given company to calculate its value. Usually, it is a combination of all of its assets, including the common stocks from the stock exchange. So far, so good; however, the stock exchange evaluation rules are pretty exciting. More specifically, the rule of how the end-of-day price calculation is done. It is based on the amount of money an individual is willing to pay for a given stock. And here is the part that must bother us – one big chunk of a given company evaluation is entirely based on people’s trust in the company. It is not based on any real-life assets such as gold, art, or real estate. It is entirely based on faith. We can even safely assume that we ll are living in a trust-based economy.

But let’s go back to loans – how do we calculate the personal wealth of people. The answer is a simple one. The same way banks calculate the evaluation of a company – aka based on all personal assets, including stocks. When wealthy individuals decide to buy something or invest in something, they have two ways of doing that – to sell assets or to get a loan.

Usually, most of them are willing to get a loan based on the current evaluation of their stocks and payback later. However, to give the loan, the bank does the review based on the willingness of someone to buy the stocks at a given price. In traditional banking, this usually triggers the central banks to issue a new amount of the local currency to provide the bank with the amount of money necessary to give the loan. So, in short, every time the bank provides a loan based on stocks, we pump new money into the system and lower down the buying power of everyone attached to the local currency.

In conclusion, most wealthy individuals prefer to finance their operations using loans instead of selling stocks at the current value. However, getting a loan increases inflation because the central banks have to issue new money to fund these loans. Another question is how much is the buying power of our modern billionaires compared to the ones in the past. For sure, most of them can not afford to finance the operations of over 1000 public libraries with their own money.