In an economy, the standard categorization of assets is divisible and non-divisible. We could categorize all FIAT currencies, gold, land, etc., into divisible assets – everything we could divide into smaller chunks. On the other hand, a non-divisible asset is an asset that we can not divide legally – for example; we can not cut a piece from a painting and sell only it. The same is true for apartments, buildings, collectibles, etc. A unique number or id usually identifies both types of assets, but assets of non-divisible kinds sometimes could only have one copy.

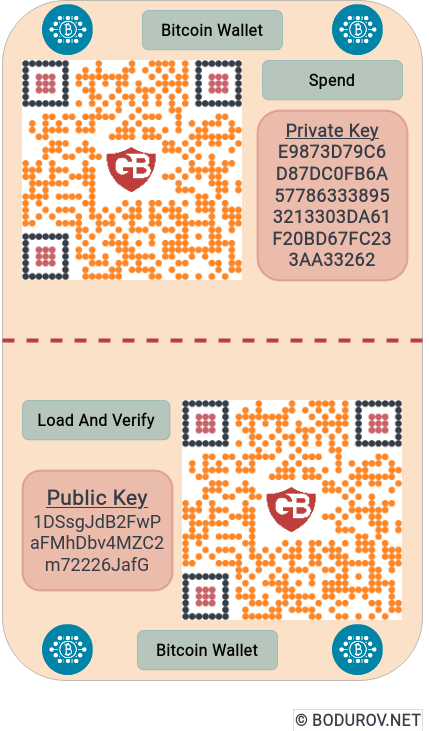

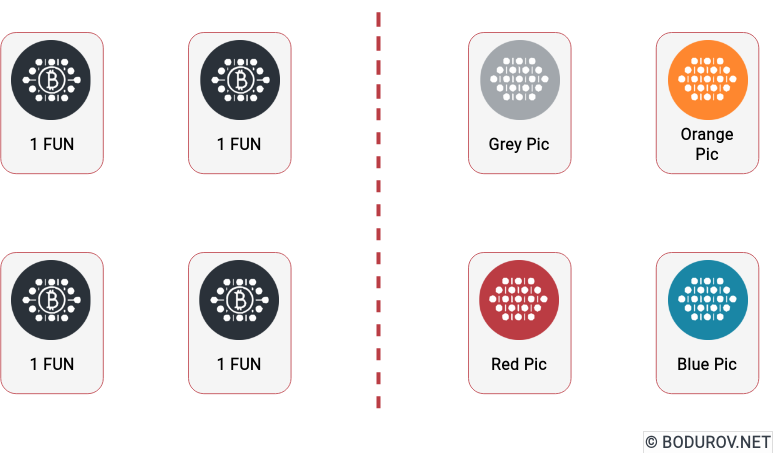

We can see many parallels if we return to the crypto world and translate between the previous paragraph and the different tokens offered by the various crypto exchanges. In crypto, we call all divisible tokens “fungible”. Examples of such tokens are bitcoins, etheriums, and any other cryptocurrency. To verify transactions over the set of these tokens, we use the nature of how blockchain networks work. Every transaction is cryptographically signed, and one transaction keeps the metadata for the tokens transfer between two or more wallets. Usually, in this metadata, we store the unique id of the divisible token (when we split the token, we typically generate a new id/number for every part of the split).

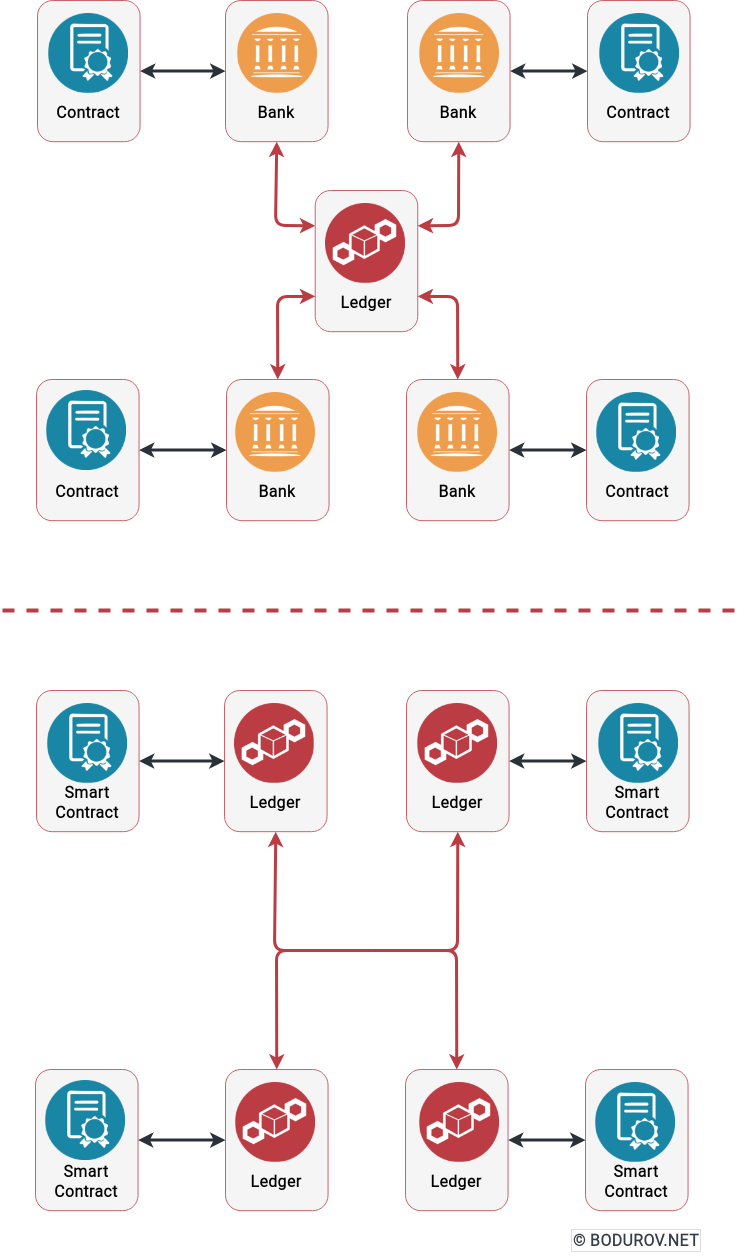

The programming logic used to implement the described set of features is called a smart contract, and it could be described as a daemon program (for people who are not aware of the terminology, this is a service program running in the background), which operations could be stored into the ledger storage and are cryptographically signed. So essentially, when we transfer tokens, we call this program and its API.

Let’s return to NFTs now. Essentially, NFT means non-fungible token and is a non-divisible asset by its logic. Every NFT has a unique ID similar to the standard tokens and could be transferred between owners. There is a slight difference that we can not divide them, and currently, the protocol does not support multiple owners of the same NFT. Additionally, unlike standard tokens, NFTs could be emitted only by manual intervention but not auto-generated by the protocol itself as rewards.

A more profound analysis of the described behavior could give us the insights that NFS was designed to replace the standard legal contract by enabling the parties to upload their deal’s metadata into the blockchain. And thus to probably avoid the use of notary or at least to digitalize their work.

But how does this transfer to digital arts and collectibles? Usually, digital art is a digital file in some format (most of the time, we speak about images, but this could be a whole game model into a video game, for example). And copying a digital file is one of the basic operations we are taught when using computers. And here comes the help from cryptography – we could easily calculate a hash of the file, generate a random id for it, and sign them from the issuer name. This way, an artist could upload their file multiple times and offer a unique NFT for every file copy.

In conclusion – NFTs’ way of working is quite promising. With some will coming from governments around the World, it could easily automize and speed up the performance of different legal frameworks. Additionally, it would increase the visibility and clarity of how they work. At the same time – unfortunately, the way use it, aka selling pictures of cats and game models, is a little bit speculative. Unfortunately, it inherits some of the disadvantages of traditional fungible tokens, especially the problem with the emission of new assets into the network.