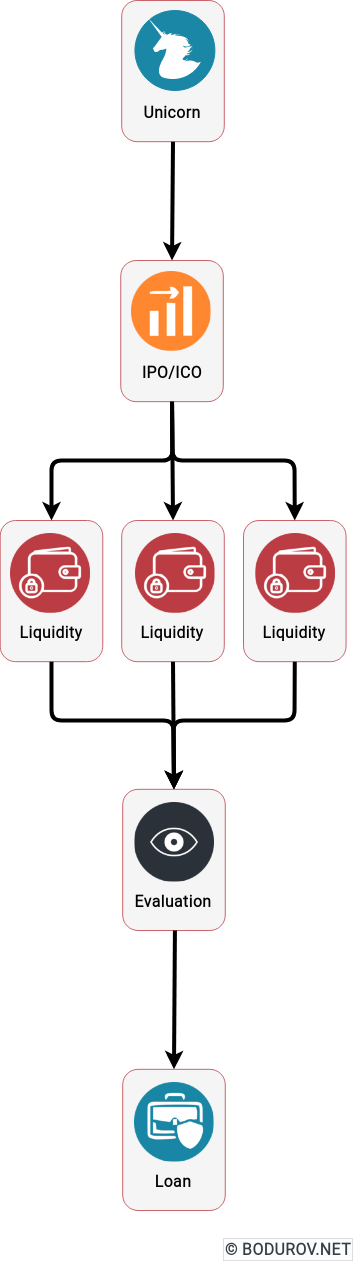

After the two weeks-long enforced COVID pause I had to endure, now I am back with the last part of the StartUp Lifecycle series. In this part, we shall speak about what happens after the Start-Up has multiple rounds of bank loans and the usual working strategy after the Start-Up has reached the IPO. Previous parts of the series you can find here and here.

Now, once the Start-Up reaches the IPO status, the modus operandi has to change a bit. The company has to prove itself as a leader in the field and acquire as many clients as possible. Usually, the founders try to balance between too many bank loans and enough income to pay for the developed infrastructure and employees. At that phase, the Start-Up is no longer “categorized” as a Start-Up but usually as a mature and more giant company. Better and more mature processes are established, and usually, the management has to find a way to delegate and distribute the management power and duties.

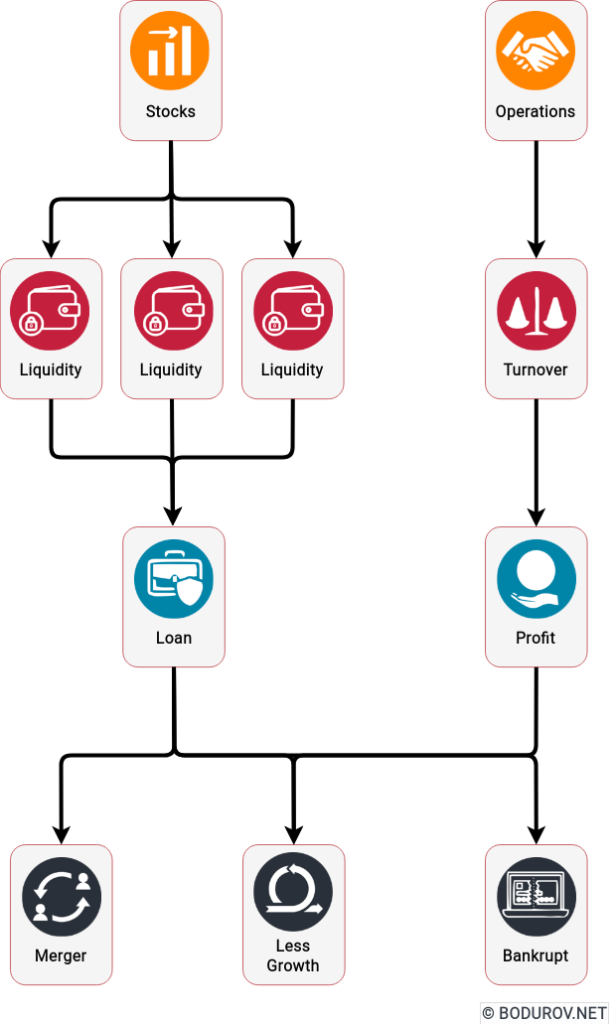

On the economic side of things, we could not expect new investments and fundings. Usually, the board of directors is trying to survive on IPO and profits. As a rule of thumb, we could expect the company to operate at a loss and cover this loss using IPO profits or bank loans. This way of operation usually gives a good long run of business execution. With this strategy, the company can survive for around 10-15 years, and during this lifespan, the company owners have three options:

- To find another company for merger or acquisition: At this stage, the company usually has enough assets and IP, which could interest another company. Mergers and acquisitions are typically categorized as successful exits and will leave founders’ reputations intact.

- To make the company run on profit: Some owners could decide to stop the company’s growth and focus on getting enough clients to keep the company on profit. That was not a rare choice in the past. However, many company owners will pursue option one because it gives them less risk in the long term.

- To fill bankrupt: As everything in our world, companies could come to an end. Balancing between shares, bank loans, and profit could be tricky sometimes and lead to erroneous results. Significantly, the share price is sometimes quite volatile and could be affected by the CEO’s matters and life choices.

In conclusion, at that stage, companies rarely fall bankrupt. Most owners and major shareholders would prefer to sell the company and its assets instead of bankrupting. At least this way, the employees usually retain their jobs and can be moved to more successful projects in the new company/structure.